In Colombia, the transfer pricing regime is crucial for companies conducting transactions with related foreign entities or within free trade zones and/or with companies located in low or no tax jurisdictions. This regime ensures that these transactions are conducted at market values, preventing price manipulation that could erode the taxable base in the country. Below, we highlight the key dates, thresholds, and obligations that companies must comply with during 2024 for fiscal year 2023.

Key Dates for Compliance Obligations

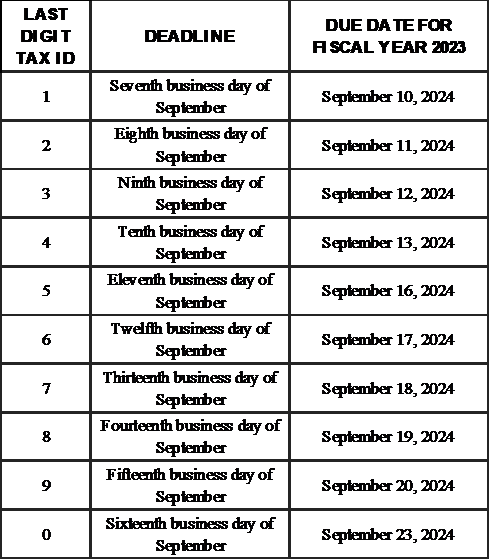

The Ministry of Finance, through Decree 2229 of December 2023, established the deadlines for complying with formal obligations related to transfer pricing for the 2023 tax year. For the submission of the Informative Return, the Country-by-Country Report Notification, the Local File, and the Master File, the deadlines were set for September each year, starting from the seventh business day of the month. Thus, for 2024, the submission dates for these formal obligations are set between September 10 and 23, 2024, depending on the last digit of the company’s NIT (Tax ID Number), as follows:

Furthermore, a single submission date for the formal obligation of the Country-by-Country Report was established for all companies. The date was set for the tenth business day of December. For 2024, the submission must be made no later than December 13, 2024.

It is important for companies to be aware of these deadlines to avoid penalties that may result from non-compliance.

Minimum Amounts for Compliance with Obligations

Companies that are income taxpayers in Colombia, that conducted transactions with related parties abroad or in free trade zones, and whose gross assets at the end of the year or tax period are equal to or greater than 100,000 UVT (Tax Value Unit) (COP 4,241,200,000 for the 2023 fiscal year) or whose gross income for the year is equal to or greater than 61,000 UVT (COP 2,587,132,000 for the 2023 tax year) must comply with the submission of the Informative Return. Taxpayers who conducted transactions with persons, companies, entities, or businesses located in non-cooperative, low or no tax jurisdictions, and preferential tax regimes are required to submit the Informative Return, regardless of whether their gross assets or gross income are below the established amounts.

Along with the Informative Return, the Country-by-Country Report Notification must also be submitted. However, taxpayers who are not required to submit the Informative Return must send the Country-by-Country Report Notification to the DIAN using a format through the email designated by the DIAN. This notification must be sent within the same deadlines stipulated for the submission of the Informative Return.

If taxpayers meet the minimum thresholds of gross assets or gross income mentioned above and conducted transactions with related foreign companies or in free trade zones for an annual cumulative amount by type of transaction equal to or greater than 45,000 UVT (COP 1,908,540,000 for the 2023 fiscal year) or conducted transactions with entities in non-cooperative, low or no tax jurisdictions, and preferential tax regimes equal to or greater than 10,000 UVT (COP 424,120,000 for the 2023 fiscal year), they must submit the Local File and the Master File, the latter required for Multinational Groups.

Importance of Specialized Advisory Services

Since compliance with the transfer pricing regime requires considerable technical precision and a deep understanding of current regulations, it is essential to have specialized advisory services. At BéndiksenLaw, we offer planning, consulting, and comprehensive assistance services to ensure that your company complies with all obligations, avoiding tax risks and penalties.

Contact us today for a consultation and ensure that your company is in full compliance with the current transfer pricing regulations in Colombia.